The World Has Changed

COVID-19 is a generational event that will impact the way people live, work and behave long after the pandemic has been controlled and a vaccine produced.

So what does that actually mean and what will the impact be on the Build to Rent (BTR) sector? It seems there is no shortage of views on this and headlines vary wildly from day to day. Suffice to say we have not been here before and the pandemic is not yet over so no one really knows for sure however, there are some inevitabilities, some certainties and some historical precedent which, when taken together, can provide a roadmap of sorts for what to expect in the coming months.

Inevitability

Recession is inevitable. However, what kind of recession is less clear. ‘V’, ‘U’, ‘L’, ‘double dip’, ‘worst since The Great Depression’ – all are on the table but what path it takes will only be obvious with hindsight. We are now well into the second month of significantly reduced market activity and the most optimistic views are that it will be mid-May before any sort of return is possible. The fact that the government has taken unprecedented action is irrefutable however the outcome of those measures is still to be determined as is, of course, the ultimate cost.

Certainty

People will still need to rent. However, consumer behaviour will have changed dramatically with a shift in priorities affecting a likely change in requirements and mindset.

It is critical the sector recognises that and adapts accordingly.

What do we know right now?

Residents expect you to help.

With the lockdown in place, reports of large waiting lists for universal credit and housing payments and people being laid off or facing some loss of income, it is inevitable that the number of people defaulting on their rent in the coming months will increase significantly.

Earlier this month Property Week reported that collection rates were as low as 44% and Shelter has warned of an ‘onslaught’ of people unable to afford their rent. Shelter’s research outlines that 1.7 million believe they will lose their jobs in the next three months (the OBR are forecasting 2m), that nearly one in four renters (24%) in England have already seen their incomes fall or lost their jobs and 23% say that losing their job will leave them unable to pay their rent immediately.

Whilst collection rates appear to be higher currently in BTR schemes, the full picture will only really be seen in the coming month/s.

Talks of a rental strike do not appear likely to result in any collective action for the time being. Nevertheless, there is increasing evidence of disquiet among renters at the lack of direct support from the government, leading to an inevitable reliance on private support from landlords.

Stories of unsupportive landlords are thankfully matched by examples of those adopting a more understanding approach. BTR operators have a real opportunity to demonstrate the very ethos the sector purports to be built upon; putting the customer first and communicating with residents in a highly empathetic way is key. Whilst policies will no doubt be in place for ‘normal times’ these are not they and the need to have a flexible case by case approach offering payment plans, rent deferrals, discounts etc. will go a long way to enhancing both reputation and brand and engendering loyalty from residents when they get back on their feet.

Pricing is key – and it will go down.

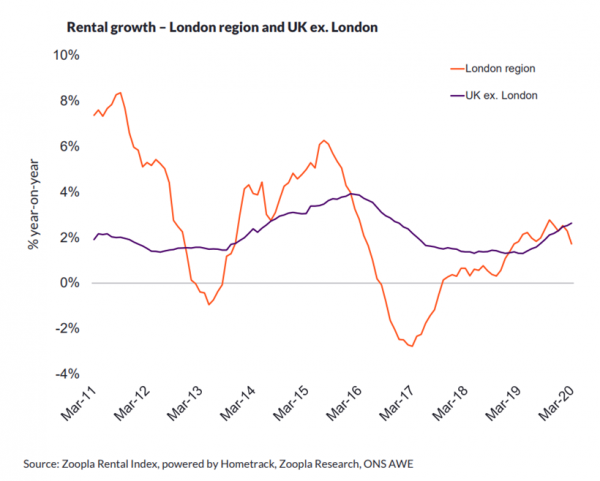

For the first time in 12 months, London’s pace of rental growth has fallen behind the rest of the UK.

Although as much to do with affordability levels in London already being at a peak before COVID-19, it is unlikely now, with the impact on people’s income, that this will go anywhere but

down in the short term.

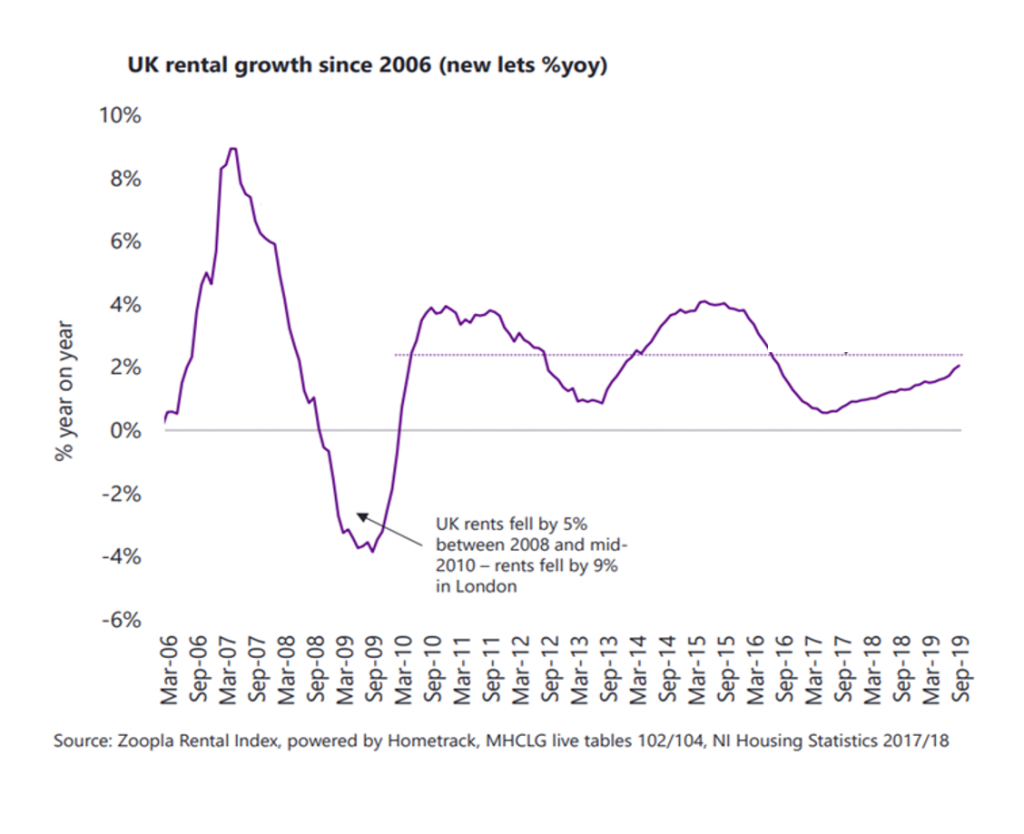

In the period following the 2008-2009 financial crash, rents in London dropped by 9%.

Given that the UK’s BTR market, in its current form at least, didn’t exist in 2008 it is useful to look at what happened in the US Multifamily market.

Here, professionally managed apartments reported rent declines in the range of -4% to -7.9%.

In addition to this, occupancies also fell to their lowest point in a decade, dropping from over 96% to just over 92% occupancy.

Clearly any direct comparison is limited as the economic impact of COVID-19 is expected to be far greater than any previous recession ever has been however, we should take some comfort from the fact that, as markets go, the residential rental sector is one of the most defensible and robust.

Short to mid-term implications

The effects will be different according to the rental price brand as decreasing demand runs coextensive to increasing supply however, we can reasonably expect the following factors to exert significant downwards pressure on rental pricing:

- The collapse of the short-let market:

The short let market has effectively imploded and as we can see from Rightmove’s data, (reporting a YoY increase of 45% in rental listings for the w/c March 16th), much of this stock is now being advertised on the long-term rental market.

- A declining sales market:

As the sales market weakens, although the usual contra-cyclical effect is increased rental demand, previous recessions have shown that where unemployment rates are high demand actually decreases while available supply expands as more households bring properties to the rental market that they would otherwise have looked to sell.

- Cost-cutting renters:

Many existing renters who have experienced a significant hit to their income will look to reduce outlays by moving back in with family members, sharing with friends or other couples, or relocating to cheaper accommodation.

Occupancy rates and ERVs will likely see the biggest decrease in schemes with high pricing as renters look to move down in scale. While theoretically this might prove a boon to the mid-value market rents, any gains will likely be negated by increasing supply and rental prices will inevitably drop across the board.

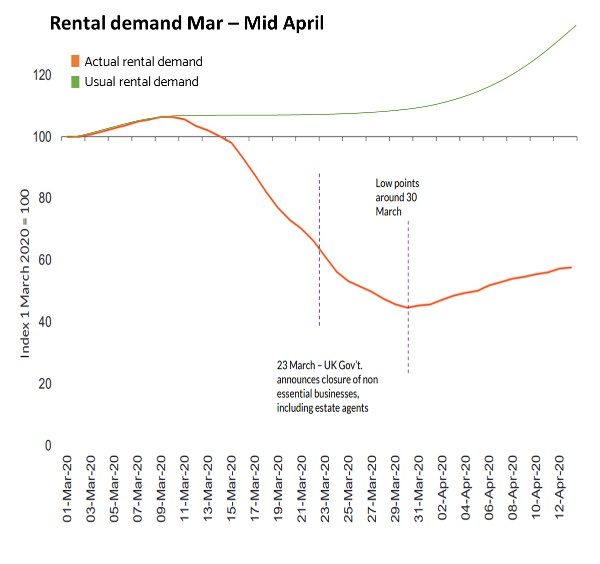

As things stand, activity in the market has started to show tentative signs of recovery although demand is still down by roughly 50% from where it would be in normal circumstances.

Demand from international students is non-existent, relocation companies aren’t relocating and for many schemes’ construction has temporarily stopped, delaying practical completion dates.

Whilst it is expected at some point international demand will return it is difficult to predict when or at what level.

Once lockdown restrictions ease activity levels will likely rise and we can expect to see a sharp spike in demand. However, it is unlikely that there will be a delayed peak season in line with normal market activity and total moves in 2020 are expected to be down by at least 25% compared with 2019.

However, it’s not all doom and gloom. There is still market activity and for those landlords and operators who adapted quickly to adopt technology to support video viewings and are able to offer flexible rental contract start dates, deals are still being done.

Here at Home Made, whilst initially there was a sharp decline in enquiries, this has subsequently picked up and we have seen a surprisingly strong pipeline of offers being made and agreed. Many renters have more time to complete a property search for moves they were already planning or are now choosing to make and are highly motivated to get ahead of the market.

The long-term implications for BTR

‘Out of adversity comes opportunity’.

The BTR sector is now perfectly placed to be able to demonstrate the value proposition of the very tenets on which it is based. The phrases ‘customer centric’ and ‘community’ have become part of the BTR bible and never before have they come into sharper focus. There are heartwarming stories from scheme to scheme of innovative resident engagement programmes, community events etc. with wellbeing and health of both residents and staff being prioritised. Operators have come together to share experiences and learnings in a spirit of camaraderie and openness not usually witnessed.

So, when the dust settles, lockdown measures are lifted and slow adjustment to whatever the ‘new normal’ looks like are made, how can the sector build upon this and what can be done to mitigate commercial losses as much as possible.

Product

Across the capital the proposition offered by BTR schemes is diverse. From heavily amenitised premium grade accommodation with on-site teams and premium rents through to mid-low grade accommodation, (often permitted development schemes) with no amenities, no onsite staff and accordingly much lower rents. Affordability (as always) will be the primary driver of consumer choice and we have already talked about the impact this will have on pricing, however, not only will renters have less money, they will also likely choose to be even more frugal with it. Uncertainty about future unemployment will be high for many and spending habits will change.

With this shift in spending will also come a shift in priorities. Many renters are realising how important the space that they inhabit has become and are identifying desirable amenities that they don’t currently have access to, (outside space, a balcony, etc.) or features that don’t really work for them (layout, room sizes, poor wi-fi, etc.) that they want to change as soon as possible.

As companionship and wellbeing has taken a higher priority there has been a surge in people looking to own pets with the Kennel Club reporting an 84% increase in the use of their ‘find a puppy’ tool. Community remains as important as ever and those who have prioritised this in their placemaking efforts will have engendered loyalty and trust. This investment now could have a strong return in the weeks and months to come.

Proposition

How the proposition is framed will now become key.

- For those that offer amenities, frame these as complimentary rather than offering them as included in the rent. This will protect your scheme against any resident feeling justified in demanding a rent reduction should these be out of action for the foreseeable or at any time in the future.

- If you have a no pets policy, consider changing it.

- If your offering doesn’t have a resident engagement programme, consider creating one. People will care a lot more about connecting with their neighbours and have ways of caring for, and engaging with, them.

- Review your building’s digital infrastructure. Working from home is essential right now but even when restrictions are relaxed it is expected many more people will choose to, so having good internet connectivity will be critical.

- Offer flexible contracts. Many renters will be concerned about the future. It is more uncertain now than it ever has been before and having the flexibility to be able to react to any future events will be something many look to secure.

Operations

The operational challenges of running a building during lockdown are immense. Whilst a lifting of lockdown conditions will see some easing of the most restrictive measures it is likely that many of the new rules will be in play for some time to come.

Anxiety will be high for many months and may never return to normal with people having much more concern over things they would not have before.

- Cleaning needs to be seen, not just done.

Whereas previously many cleaning routines would have been done in the twilight hours now residents will be reassured by seeing it undertaken and to a very high standard. Residents’ emotional reactions will be heightened and ensuring steps are taken to account for this will be important.

- Emergency procedures should all be reviewed.

Whilst eventually this crisis will be a memory, the next black swan could take place without warning again and having a robust plan of action that can be deployed quickly will be critical. Reviewing supply chains, emergency communication methods with all staff and residents etc. etc.

- Staffing

Many operators have taken steps to move some of the on-site staff into the building and in the US this is commonplace even in normal conditions. Factoring this into the staffing model should become standard as these staff become the investor’s key workers. Review salaries and shift patterns to reflect this and ensure all safety protection measures are in place (PPE/CCTV/lone worker devices) for any staff that will need them.

For any staff that cannot live on-site but will travel to the building consider providing safe transport so they can commute without needing to use public transport.

Marketing

In the spirit of ‘everything under review’ there is no doubt the place this will count the most is in marketing.

Everything we once knew to be true is no more and those that will capitalise the most from demand in the market will be those that adapt the fastest.

Right now, outdoor above the line (ATL) advertising is redundant. With footfall currently over 90% down that’s obvious, however the ROI (which is always difficult to establish here anyway) will be much lower in the coming months as footfall will remain down month on month.

Portal traffic is also down to record lows with Rightmove and Zoopla ~50% down, and search traffic for keywords such as “Flats to rent in London” is down by 67%.

However, there are big gains to be had from through the line (TTL) strategies, with usage per day on social channels such as all Facebook apps up by 67%. This means it is the easiest way to be exposed to most renters, or soon-to-be renters right now.

Consumption of other online content has also, unsurprisingly, increased significantly with video services and newspapers recording dramatic spikes in traffic.

“Video viewings” and “walkthroughs” have seen a massive surge in search which is testament to there being demand in the market but evidence that it is coming from a different place. The restrictions on people’s movement have obviously driven this change but the emerging significance of the video viewing is not just temporary. Even when lockdown measures are lifted many people will be anxious about travelling and will look to use digital solutions to help them filter their search. When international demand returns many will look to properties where they can view remotely to help make decisions. Our experience is that they are a highly effective tool (when used correctly) and provide an invaluable way of establishing trust and confidence that ultimately secures offers.

As far as the traditional agency model goes the future is very uncertain for many.

Our research showed that two out of three traditional agencies currently aren’t picking up the phone or processing any incoming enquiries on listings and it is predicted that many high street agents will need to cut costs and close branches or shut down altogether. With estate and letting agents already among the fastest closing businesses on the high street, their role in the lease up of BTR schemes is uncertain at best.

The priority for all investors and operators will be speed of lease up. This shouldn’t be at the expense of finding the quality applicant but the competition for these residents is going to be high. In order to achieve the volume of enquiries needed to achieve this it will be those who adopt the best, newly adapted marketing strategies that will see the biggest wins.

Knowing your CAC will be essential. Costs will need to be kept as low as possible and returns as high. Understanding exactly what each channel returns and the value proposition will be critical, and many will need to review the value of ATL strategies altogether.

Summary

While the crisis is far from over, as a sector we are well placed to adapt to and succeed under new market conditions. It is encouraging to know that the comparable US Multifamily sector was one of the fastest in the property industry to recover following the financial crash and ultimately experienced the longest period of sustained rental growth.

People will still, and always, need to rent and the opportunity to enhance the value perception of the ethos of Build to Rent has never been higher.

We are, as always, here to help and if you want to speak to us about how we can support the lease up of your scheme get in touch with us today. After all, “A good plan violently executed now is better than a perfect plan executed next week.” George S. Patton